Worldwide Disclosure Facility (WDF)

Offshore Disclosures

Our founder has over 20 years’ experience working in HMRC as well as having professional tax qualifications. All of our staff have either HMRC or an accountancy background.

The Worldwide Disclosure Facility (WDF) is a HMRC process for those wishing to make a disclosure of offshore income, money, investments, gains or assets.

Whether you have offshore income, gains, investments, assets and need to resolve your tax affairs with HMRC, our developed guide focussed on the Worldwide Disclosure Facility (WDF) will go into detail and give you an understanding of how it works. The WDF differs from previous offshore disclosure facilities, all of which are now closed.

Here at Lionhart Tax, we assist numerous clients with their WDF disclosure on a day-to-day basis and are equipped with knowledge to answer any queries you may have regarding WDF.

Our founder is ex HMRC with over 20 years experience including being the project manager for the Worldwide Disclosure Facility during his time in HMRC. He was instrumental in devising not just the letter HMRC issues but also various procedures and processes being put in place which are still used by HMRC.

Contact us now on 0114 400 0192 for information or assistance on enquiries or dealing with your WDF disclosure today!

Our staff are multilingual and you can speak to us in English, Punjabi and Urdu amongst other languages.

Frequently Asked Questions

With over 100 countries from all around the world, having come together committed to exchanging information on a multilateral basis under the Organisation for Economic Co-operation and Development’s (OECD) Common Reporting Standard (CRS). CRS ultimately aims to control and cut down on the use of offshore jurisdictions to facilitate tax evasion.

From the 5th of September 2016 the WDF became available, which at that point the Worldwide Disclosure Facility replaced all disclosure Schemes which were previously put in place, such as the Liechtenstein Disclosure Facility (LDF) and the Crown Dependencies Disclosure Facilities (CDDF).

The Liechtenstein Disclosure Facility became obsolete by the end of 2015. Previous to 2016 the Liechtenstein Disclosure Facility gave UK residents, who may have undeclared tax liabilities, the opportunity to settle any outstanding tax affairs with HMRC. As well as offering beneficial terms and immunity from prosecution. Although the WDF as of now does not offer these terms, however, it would still benefit you to disclose in a timely manner to avoid any possible penalties. It can also reduce the possibility of criminal prosecution even though there is no immunity guaranteed.

Within the Common Reporting Standard (CRS), HMRC will receive details about taxpayers regarding offshore income or gains from over 100 foreign jurisdictions. Therefore, before HMRC start an enquiry or investigation, it is more favourable to disclose any offshore income or assets to HMRC, particularly to reduce the possibility of a criminal prosecution.

The Worldwide Disclosure Facility (WDF) was introduced on the 5th September 2016, and can be accessed by anyone who has any UK tax liability to disclose, which is in relation to an offshore income or gain.

When referring to an offshore issue, this can include unpaid or omitted tax relating to:

- Income which is sourced from outside the UK

- Assets which are been held outside the UK

- Activities which are carried out mainly outside the UK

- Funds which are in relation to unpaid UK tax, that were transferred or owned outside the UK

- Anything effected as if it were income, assets or activities of a kind which are described in any of the points stated above.

If at any point HMRC suspects that any assets or funds which are included within your disclosure in any way are made up of criminal property, then they have rights to refuse any application made by you to take part in the Worldwide Disclosure Facility.

If for any reason you’re questioning if you’ll meet the eligibility criteria for the facility, then it is advised to seek professional advice. If you do not reside in the UK, you are still entitled to make a disclosure if you meet the eligibility criteria which is stated above.

- WDF applies to all tax years leading up to and including the current tax year.

- If HMRC has contacted you regarding your tax return for the current year or any tax year from 2016/17 onwards which is still outstanding, then you must complete the return and not include these tax years within the disclosure.

Your behaviour will be self-assessed in order to indicate the number of years you will need to disclose. This could be four, six or up to 20 years.

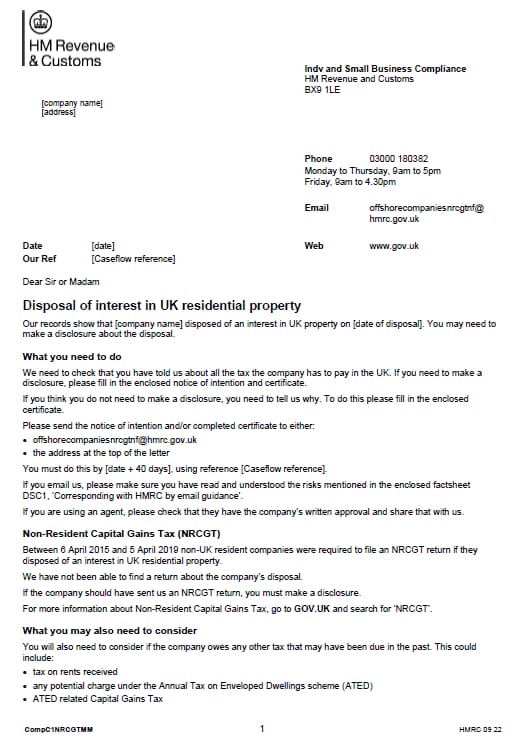

HMRC will have sent a ‘nudge’ letter to many individuals who fall under its ‘at risk’ population. More of these letters in particular are expected during the course of 2022 and in the near future.

The purpose of the letter is primarily to:

- Inform that HMRC have information on an offshore asset help by the individual

- Request confirmation that the individuals’ taxes affairs are up to date

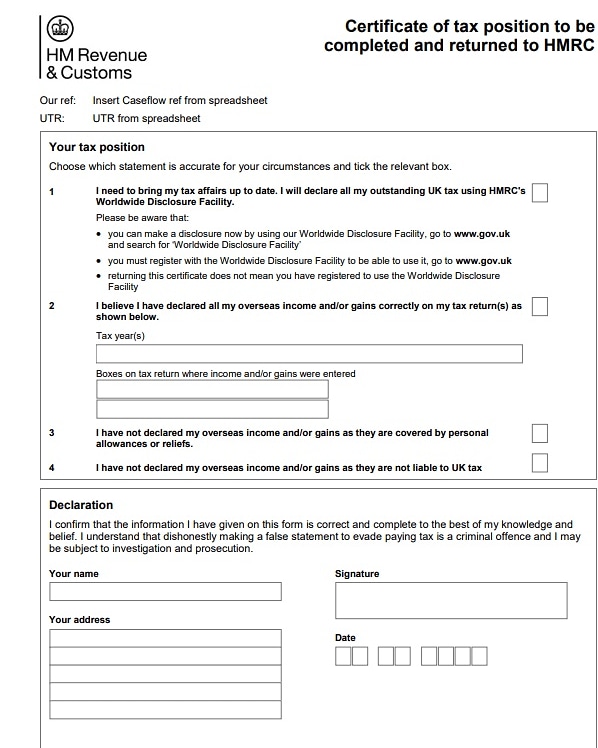

- Request for a signed declaration that they know of no inaccuracies in their returns or ask for confirmation that a tax disclosure will now be made.

The first thing to do, as with any other case is to take it seriously. HMRC have potentially found a problem with your offshore tax affairs, which can go back as far as 20 years. If these queries are not responded to HMRC will escalate this further. This could potentially also lead to you being investigated criminally.

Secondly, if you are unsure what the offshore tax matter HMRC is referring to our suggestion is to contact HMRC. They may be able to disclose information in regard to the asset in question, which will help you pinpoint the fault in your tax affairs. Keep in mind it is not certain they will share any information with you.

Thirdly, take the opportunity to work alongside a tax expert who will help review your offshore assets and ownership structures. This can mean that there are no issues that will need disclosing and everything is as it should be. If there is a disclosure to be made, Lionhart Tax can assist you with this.

- Remember: a false declaration could be a criminal offence. Careful consideration and professional advice are essential before responding to a nudge letter, or making a disclosure.

The Lionhart Tax team has extensive experience of advising on offshore tax, Requirement To Correct (RTC) compliance and disclosures to HMRC including the WDF (the Worldwide Disclosure Facility) which is a HMRC process enabling taxpayers to correct past irregularities in connection with offshore matters.

HMRC has issued (and is continuing to issue) other letters to: - tenants and landlords regarding UK properties owned overseas, asking for information to be provided.

- those suspected of having offshore investment funds, asking people to check Excess Reporting Income and Offshore Income and gains have been declared correctly.

If you have received this letter and need help in this regard, feel free to contact us on 0114 44000192

Definitely not. You should disclose this as soon as possible. If you act first, potentially you will face lower penalties. You are also reducing the chances of HMRC opening a criminal investigation or arrest. Therefore, your future affairs can be in order, and you will avoid potential penalties and interest.

What does the (WDF) process involve?

Summary of the WDF Process:

- Make HMRC aware of the intention to disclose through the Digital Disclosure Service (DDS).

- A disclosure should be produced within a period of 90 days including calculations of the additional tax, interest and penalties due. This will all be submitted through the DDS.

- Within the time of the disclosure, the taxpayer will be asked to self-assess their behaviour. This is a practical matter which will impact on the penalties and will determine the number of years that the disclosure will cover.

- Any technical matters which will affect the disclosure must be disclosed. This may include exploring residence and domicile status.

- In exceptional circumstances, it is possible that advance clarification may be required in respect of complex or contentious issues.

- As part of the disclosure, the taxpayer will be required to enter the maximum value of assets which have been held outside the UK over the last five years including cash, investments, and personal goods such as jewellery.

- Payments must be made when the submission is due; however a ‘time to pay’ may be agreed if appropriate.